Statistical Thinking in Python (Part 1)

Introduction

- Course: DataCamp: Statistical Thinking in Python (Part 1)

- This notebook was created as a reproducible reference.

- The material is from the course, and I completed the exercises.

- If you find the content beneficial, consider a DataCamp Subscription.

Course Description

Learn the principles of statistical inference to make clear, succinct conclusions from data. This course builds the foundation needed to think statistically and understand your data using Python-based tools. By the end of the course, you will be able to analyze data and draw meaningful conclusions efficiently.

Synopsis

Graphical Exploratory Data Analysis

- Objectives:

- Understand the importance of visualizing data.

- Learn various graphical techniques to explore data patterns, including histograms, box plots, scatter plots, swarm plots, and ECDFs.

- Methods:

- Use histograms to display distributions.

- Create box plots to visualize data spread and detect outliers.

- Generate scatter plots to observe relationships between variables.

- Utilize swarm plots for detailed distribution views.

- Apply ECDFs (Empirical Cumulative Distribution Functions) to understand data distributions.

- Findings:

- Graphical methods reveal underlying patterns, distributions, and potential outliers.

- Visualization aids in understanding relationships between variables and distributions of data.

Quantitative Exploratory Data Analysis

- Objectives:

- Perform numerical summaries of data.

- Understand measures of central tendency and variability.

- Methods:

- Calculate mean, median, variance, and standard deviation.

- Use pandas for descriptive statistics and data summarization.

- Findings:

- Quantitative summaries provide a numerical snapshot of data.

- Measures of central tendency and variability help in understanding data distribution.

Thinking Probabilistically: Discrete Variables

- Objectives:

- Develop a probabilistic mindset for analyzing discrete data.

- Understand probability mass functions and cumulative distribution functions for discrete variables.

- Methods:

- Calculate probabilities for discrete events.

- Use numpy for generating random variables and computing distributions.

- Findings:

- Probabilistic thinking aids in predicting the likelihood of discrete outcomes.

- Understanding distributions is key to analyzing discrete data.

Thinking Probabilistically: Continuous Variables

- Objectives:

- Apply probabilistic thinking to continuous data.

- Understand probability density functions and cumulative distribution functions for continuous variables.

- Methods:

- Use numpy and scipy to work with continuous random variables.

- Compute and visualize continuous distributions.

- Findings:

- Continuous distributions provide insights into the likelihood of continuous outcomes.

- Analyzing continuous data requires understanding of probability density functions.

Imports

1

2

3

4

5

6

7

8

9

10

11

import pandas as pd

import matplotlib.pyplot as plt

from matplotlib.patches import Rectangle

import numpy as np

from pprint import pprint as pp

import csv

from pathlib import Path

import seaborn as sns

from scipy.stats import binom

from sklearn.datasets import load_iris

Pandas Configuration Options

1

2

3

pd.set_option('display.max_columns', 200)

pd.set_option('display.max_rows', 300)

pd.set_option('display.expand_frame_repr', True)

Data Files Location

- Most data files for the exercises can be found on the course site

Data File Objects

1

2

3

4

5

data = Path.cwd() / 'data' / '2019-07-10_statistical_thinking_1'

elections_all_file = data / '2008_all_states.csv'

elections_swing_file = data / '2008_swing_states.csv'

belmont_file = data / 'belmont.csv'

sol_file = data / 'michelson_speed_of_light.csv'

Iris Data Set

1

2

3

4

5

6

7

8

9

10

11

iris = load_iris()

iris_df = pd.DataFrame(data=np.c_[iris['data'], iris['target']], columns=iris['feature_names'] + ['target'])

def iris_typing(x):

types = {0.0: 'setosa',

1.0: 'versicolour',

2.0: 'virginica'}

return types[x]

iris_df['species'] = iris_df.target.apply(iris_typing)

iris_df.head()

| sepal length (cm) | sepal width (cm) | petal length (cm) | petal width (cm) | target | species | |

|---|---|---|---|---|---|---|

| 0 | 5.1 | 3.5 | 1.4 | 0.2 | 0.0 | setosa |

| 1 | 4.9 | 3.0 | 1.4 | 0.2 | 0.0 | setosa |

| 2 | 4.7 | 3.2 | 1.3 | 0.2 | 0.0 | setosa |

| 3 | 4.6 | 3.1 | 1.5 | 0.2 | 0.0 | setosa |

| 4 | 5.0 | 3.6 | 1.4 | 0.2 | 0.0 | setosa |

Graphical exploratory data analysis

Look before you leap! A very important proverb, indeed. Prior to diving in headlong into sophisticated statistical inference techniques, you should first explore your data by plotting them and computing simple summary statistics. This process, called exploratory data analysis, is a crucial first step in statistical analysis of data. So it is a fitting subject for the first chapter of Statistical Thinking in Python.

Introduction to exploratory data analysis

- Exploring the data is a crucial step of the analysis.

- Organizing

- Plotting

- Computing numerical summaries

- This idea is known as exploratory data analysis (EDA)

- “Exploratory data analysis can never be the whole story, but nothing else can serve as the foundation stone.” - John Tukey

1

2

swing = pd.read_csv(elections_swing_file)

swing.head()

| state | county | total_votes | dem_votes | rep_votes | dem_share | |

|---|---|---|---|---|---|---|

| 0 | PA | Erie County | 127691 | 75775 | 50351 | 60.08 |

| 1 | PA | Bradford County | 25787 | 10306 | 15057 | 40.64 |

| 2 | PA | Tioga County | 17984 | 6390 | 11326 | 36.07 |

| 3 | PA | McKean County | 15947 | 6465 | 9224 | 41.21 |

| 4 | PA | Potter County | 7507 | 2300 | 5109 | 31.04 |

- The raw data isn’t particularly informative

- We could start computing parameters and their confidence intervals and do hypothesis test…

- …however, we should graphically explore the data first

Tukey’s comments on EDA

Even though you probably have not read Tukey’s book, I suspect you already have a good idea about his viewpoint from the video introducing you to exploratory data analysis. Which of the following quotes is not directly from Tukey?

- Exploratory data analysis is detective work.

- There is no excuse for failing to plot and look.

- The greatest value of a picture is that it forces us to notice what we never expected to see.

- It is important to understand what you can do before you learn how to measure how well you seem to have done it.

Often times EDA is too time consuming, so it is better to jump right in and do your hypothesis tests.

Advantages of graphical EDA

Which of the following is not true of graphical EDA?

- It often involves converting tabular data into graphical form.

- If done well, graphical representations can allow for more rapid interpretation of data.

A nice looking plot is always the end goal of a statistical analysis.- There is no excuse for neglecting to do graphical EDA.

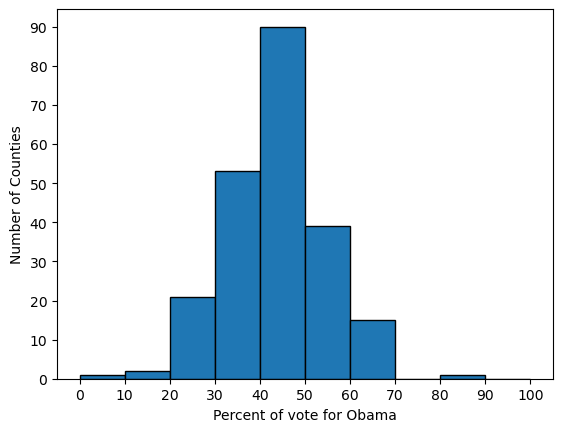

Plotting a histogram

- always label the axes

1

2

3

4

5

6

7

bin_edges = [x for x in range(0, 110, 10)]

plt.hist(x=swing.dem_share, bins=bin_edges, edgecolor='black')

plt.xticks(bin_edges)

plt.yticks(bin_edges[:-1])

plt.xlabel('Percent of vote for Obama')

plt.ylabel('Number of Counties')

plt.show()

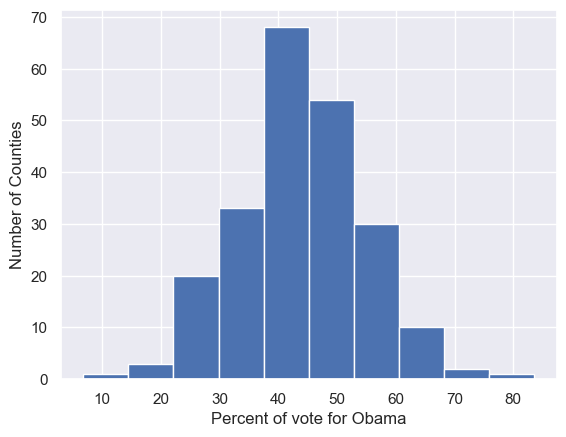

Seaborn

1

2

import seaborn as sns

sns.set()

1

2

3

4

plt.hist(x=swing.dem_share)

plt.xlabel('Percent of vote for Obama')

plt.ylabel('Number of Counties')

plt.show()

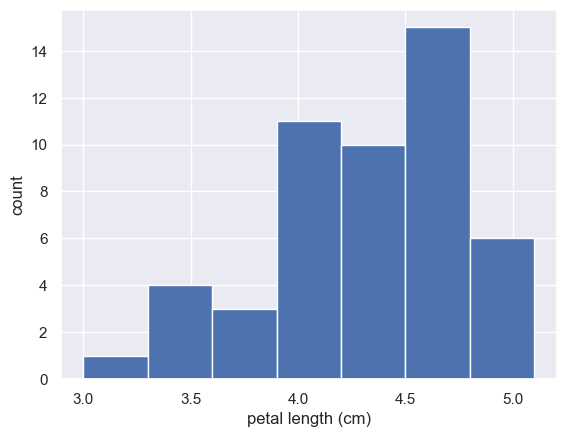

Plotting a histogram of iris data

For the exercises in this section, you will use a classic data set collected by botanist Edward Anderson and made famous by Ronald Fisher, one of the most prolific statisticians in history. Anderson carefully measured the anatomical properties of samples of three different species of iris, Iris setosa, Iris versicolor, and Iris virginica. The full data set is available as part of scikit-learn. Here, you will work with his measurements of petal length.

Plot a histogram of the petal lengths of his 50 samples of Iris versicolor using matplotlib/seaborn’s default settings. Recall that to specify the default seaborn style, you can use sns.set(), where sns is the alias that seaborn is imported as.

The subset of the data set containing the Iris versicolor petal lengths in units of centimeters (cm) is stored in the NumPy array versicolor_petal_length.

In the video, Justin plotted the histograms by using the pandas library and indexing the DataFrame to extract the desired column. Here, however, you only need to use the provided NumPy array. Also, Justin assigned his plotting statements (except for plt.show()) to the dummy variable _. This is to prevent unnecessary output from being displayed. It is not required for your solutions to these exercises, however it is good practice to use it. Alternatively, if you are working in an interactive environment such as a Jupyter notebook, you could use a ; after your plotting statements to achieve the same effect. Justin prefers using _. Therefore, you will see it used in the solution code.

Instructions

- Import

matplotlib.pyplotandseabornas their usual aliases (pltandsns). - Use

seabornto set the plotting defaults. - Plot a histogram of the Iris versicolor petal lengths using

plt.hist()and the provided NumPy arrayversicolor_petal_length. - Show the histogram using

plt.show().

1

versicolor_petal_length = iris_df['petal length (cm)'][iris_df.species == 'versicolour']

1

2

plt.hist(versicolor_petal_length)

plt.show()

Axis labels!

In the last exercise, you made a nice histogram of petal lengths of Iris versicolor, but you didn’t label the axes! That’s ok; it’s not your fault since we didn’t ask you to. Now, add axis labels to the plot using plt.xlabel() and plt.ylabel(). Don’t forget to add units and assign both statements to _. The packages matplotlib.pyplot and seaborn are already imported with their standard aliases. This will be the case in what follows, unless specified otherwise.

Instructions

- Label the axes. Don’t forget that you should always include units in your axis labels. Your y-axis label is just

'count'. Your x-axis label is'petal length (cm)'. The units are essential! - Display the plot constructed in the above steps using

plt.show().

1

2

3

4

plt.hist(versicolor_petal_length)

plt.xlabel('petal length (cm)')

plt.ylabel('count')

plt.show()

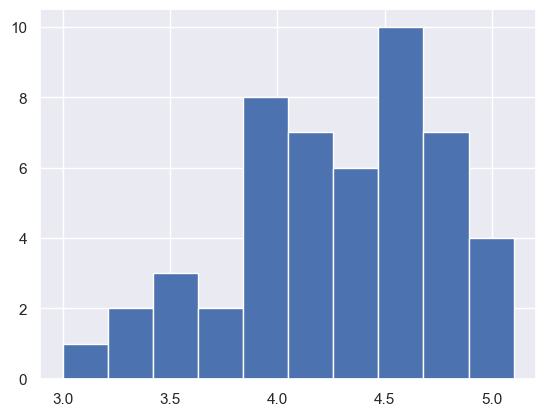

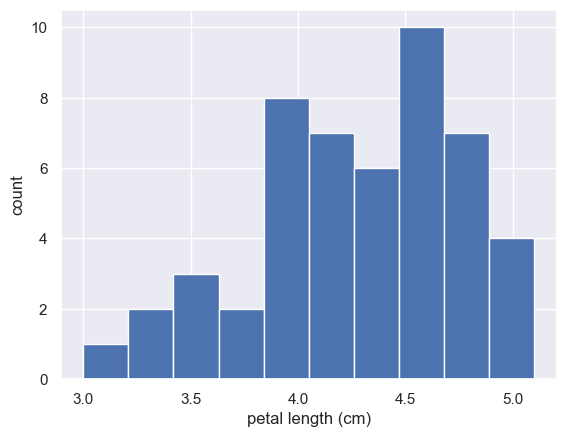

Adjusting the number of bins in a histogram

The histogram you just made had ten bins. This is the default of matplotlib. The “square root rule” is a commonly-used rule of thumb for choosing number of bins: choose the number of bins to be the square root of the number of samples. Plot the histogram of Iris versicolor petal lengths again, this time using the square root rule for the number of bins. You specify the number of bins using the bins keyword argument of plt.hist().

The plotting utilities are already imported and the seaborn defaults already set. The variable you defined in the last exercise, versicolor_petal_length, is already in your namespace.

Instructions

- Import

numpyasnp. This gives access to the square root function,np.sqrt(). - Determine how many data points you have using

len(). - Compute the number of bins using the square root rule.

- Convert the number of bins to an integer using the built in

int()function. - Generate the histogram and make sure to use the

binskeyword argument. - Hit ‘Submit Answer’ to plot the figure and see the fruit of your labors!

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

# Compute number of data points: n_data

n_data = len(versicolor_petal_length)

# Number of bins is the square root of number of data points: n_bins

n_bins = np.sqrt(n_data)

# Convert number of bins to integer: n_bins

n_bins = int(n_bins)

# Plot the histogram

_ = plt.hist(versicolor_petal_length, bins=n_bins)

# Label axes

_ = plt.xlabel('petal length (cm)')

_ = plt.ylabel('count')

# Show histogram

plt.show()

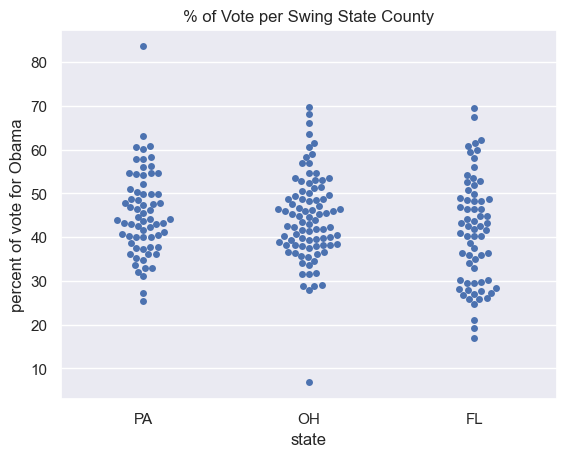

Plotting all of your data: Bee swarm plots

- Binning Bias: The same data may be interpreted differently depending on choice of bins

- Additionally, all of the data isn’t being plotted; the precision of the actual data is lost in the bins

- These issues can be resolved with swarm plots

- Point position along the y-axis is the quantitative information

- The data are spread in x to make them visible, but their precise location along the x-axis is unimportant

- No binning bias and all the data are displayed.

- Seaborn & Pandas

1

2

3

4

5

sns.swarmplot(x='state', y='dem_share', data=swing)

plt.xlabel('state')

plt.ylabel('percent of vote for Obama')

plt.title('% of Vote per Swing State County')

plt.show()

Bee swarm plot

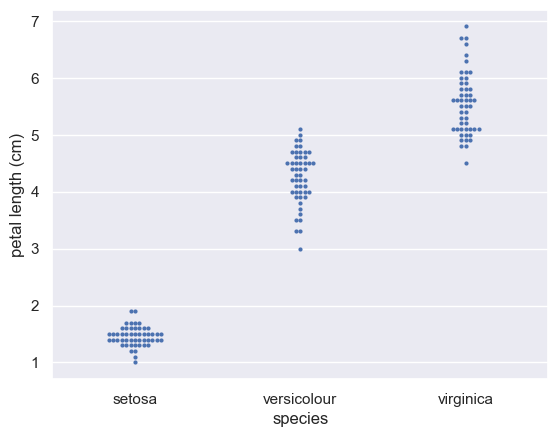

Make a bee swarm plot of the iris petal lengths. Your x-axis should contain each of the three species, and the y-axis the petal lengths. A data frame containing the data is in your namespace as df.

For your reference, the code Justin used to create the bee swarm plot in the video is provided below:

1

2

3

4

_ = sns.swarmplot(x='state', y='dem_share', data=df_swing)

_ = plt.xlabel('state')

_ = plt.ylabel('percent of vote for Obama')

plt.show()

In the IPython Shell, you can use sns.swarmplot? or help(sns.swarmplot) for more details on how to make bee swarm plots using seaborn.

Instructions

- In the IPython Shell, inspect the DataFrame

dfusingdf.head(). This will let you identify which column names you need to pass as thexandykeyword arguments in your call tosns.swarmplot(). - Use

sns.swarmplot()to make a bee swarm plot from the DataFrame containing the Fisher iris data set,df. The x-axis should contain each of the three species, and the y-axis should contain the petal lengths. - Label the axes.

- Show your plot.

1

2

3

4

sns.swarmplot(x='species', y='petal length (cm)', data=iris_df, size=3)

plt.xlabel('species')

plt.ylabel('petal length (cm)')

plt.show()

Interpreting a bee swarm plot

Which of the following conclusions could you draw from the bee swarm plot of iris petal lengths you generated in the previous exercise? For your convenience, the bee swarm plot is regenerated and shown to the right.

Instructions

Possible Answers

- All I. versicolor petals are shorter than I. virginica petals.

- I. setosa petals have a broader range of lengths than the other two species.

- **I. virginica petals tend to be the longest, and I. setosa petals tend to be the shortest of the three species.**

- I. versicolor is a hybrid of I. virginica and I. setosa.

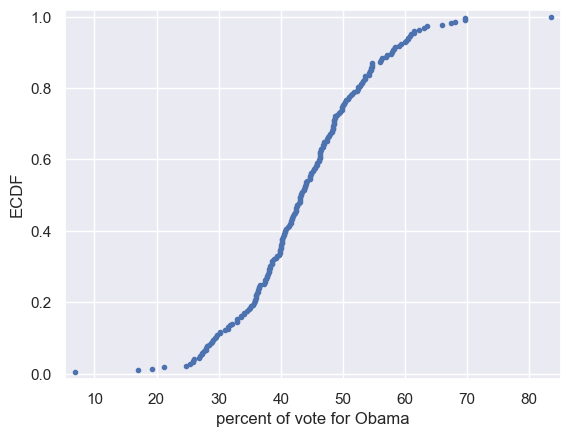

Plotting all of your data: Empirical cumulative distribution functions

- Empirical Distribution Function

- Empirical Distribution Function / Empirical CDF

- An empirical cumulative distribution function (also called the empirical distribution function, ECDF, or just EDF) and a cumulative distribution function are basically the same thing; they are both probability models for data. While a CDF is a hypothetical model of a distribution, the ECDF models empirical (i.e. observed) data. To put this another way, **the ECDF is the probability distribution you would get if you sampled from your sample, instead of the population**. Lets say you have a set of experimental (observed) data $x_{1},x_{2},\,\ldots\,x_{n}$. The EDF will give you the fraction of sample observations less than or equal to a particular value of $x$.

- More formally, if you have a set of order statistics ($y_{1}<y_{2}<\ldots<y_{n}$) from an observed random sample, then the empirical distribution function is defined as a sum of iid random variables:

- \(\hat{F}_{n}(t)=\frac{\text{number of elements in the sample \(\leq t\)}}{n}=\frac{1}{n}\sum_{i=1}^n 1_{X_{i}\leq t}\)

- Where $1_{A}$ = the indicator of event $A$.

- x-value of an ECDF is the quantity being measured

- y-value is the fraction of data points that have a value smaller than the corresponding x-value

- Shows all the data and gives a complete picture of how the data are distributed

1

2

3

4

5

6

7

8

9

x = np.sort(swing['dem_share'])

y = np.arange(1, len(x)+1) / len(x)

plt.plot(x, y, marker='.', linestyle='none')

plt.xlabel('percent of vote for Obama')

plt.ylabel('ECDF')

plt.margins(0.02) # keep data off plot edges

plt.show()

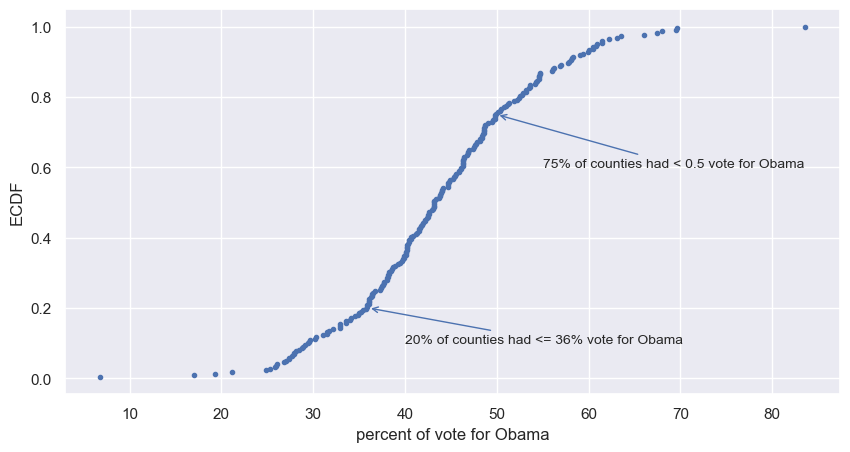

add annotations

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

fig, ax = plt.subplots(figsize=(10, 5))

ax.margins(0.05) # Default margin is 0.05, value 0 means fit

x = np.sort(swing['dem_share'])

y = np.arange(1, len(x)+1) / len(x)

ax.plot(x, y, marker='.', linestyle='none')

plt.xlabel('percent of vote for Obama')

plt.ylabel('ECDF')

ax.annotate('20% of counties had <= 36% vote for Obama', xy=(36, .2),

xytext=(40, 0.1), fontsize=10, arrowprops=dict(arrowstyle="->", color='b'))

ax.annotate('75% of counties had < 0.5 vote for Obama', xy=(50, .75),

xytext=(55, 0.6), fontsize=10, arrowprops=dict(arrowstyle="->", color='b'))

plt.show()

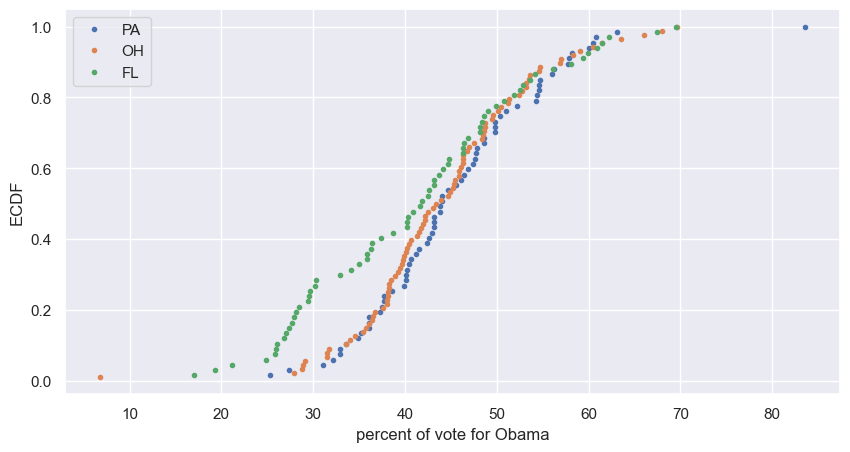

plot multiple ECDFs

1

2

3

4

5

6

7

8

9

10

11

12

13

fig, ax = plt.subplots(figsize=(10, 5))

ax.margins(0.05) # Default margin is 0.05, value 0 means fit

for state in swing.state.unique():

x = np.sort(swing['dem_share'][swing.state == state])

y = np.arange(1, len(x)+1) / len(x)

ax.plot(x, y, marker='.', linestyle='none', label=state)

plt.xlabel('percent of vote for Obama')

plt.ylabel('ECDF')

plt.legend()

plt.show()

Computing the ECDF

In this exercise, you will write a function that takes as input a 1D array of data and then returns the x and y values of the ECDF. You will use this function over and over again throughout this course and its sequel. ECDFs are among the most important plots in statistical analysis. You can write your own function, foo(x,y) according to the following skeleton:

1

2

3

4

def foo(a,b):

"""State what function does here"""

# Computation performed here

return x, y

The function foo() above takes two arguments a and b and returns two values x and y. The function header def foo(a,b): contains the function signature foo(a,b), which consists of the function name, along with its parameters. For more on writing your own functions, see DataCamp’s course Python Data Science Toolbox (Part 1)!

Instructions

- Define a function with the signature

ecdf(data). Within the function definition,- Compute the number of data points,

n, using thelen()function. - The x-values are the sorted data. Use the

np.sort()function to perform the sorting. - The y data of the ECDF go from

1/nto1in equally spaced increments. You can construct this usingnp.arange(). Remember, however, that the end value innp.arange()is not inclusive. Therefore,np.arange()will need to go from1ton+1. Be sure to divide this byn. - The function returns the values

xandy.

- Compute the number of data points,

def ecdf()

1

2

3

4

5

6

7

8

9

10

11

12

def ecdf(data):

"""Compute ECDF for a one-dimensional array of measurements."""

# Number of data points: n

n = len(data)

# x-data for the ECDF: x

x = np.sort(data)

# y-data for the ECDF: y

y = np.arange(1, n+1) / n

return x, y

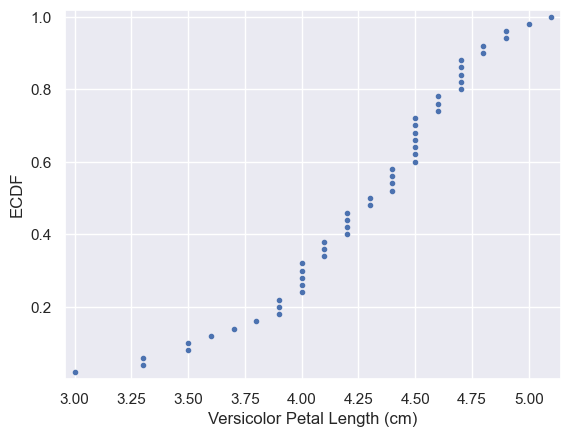

Plotting the ECDF

You will now use your ecdf() function to compute the ECDF for the petal lengths of Anderson’s Iris versicolor flowers. You will then plot the ECDF. Recall that your ecdf() function returns two arrays so you will need to unpack them. An example of such unpacking is x, y = foo(data), for some function foo().

Instructions

- Use

ecdf()to compute the ECDF ofversicolor_petal_length. Unpack the output intox_versandy_vers. - Plot the ECDF as dots. Remember to include

marker = '.'andlinestyle = 'none'in addition tox_versandy_versas arguments insideplt.plot(). - Label the axes. You can label the y-axis

'ECDF'. - Show your plot.

1

2

3

4

5

6

7

8

9

10

11

12

13

# Compute ECDF for versicolor data: x_vers, y_vers

x, y = ecdf(versicolor_petal_length)

# Generate plot

plt.plot(x, y, marker='.', linestyle='none')

# Label the axes

plt.xlabel('Versicolor Petal Length (cm)')

plt.ylabel('ECDF')

# Display the plot

plt.margins(0.02) # keep data off plot edges

plt.show()

Comparison of ECDFs

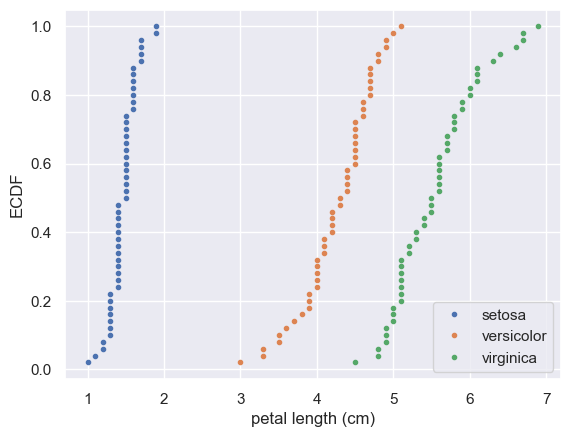

ECDFs also allow you to compare two or more distributions (though plots get cluttered if you have too many). Here, you will plot ECDFs for the petal lengths of all three iris species. You already wrote a function to generate ECDFs so you can put it to good use!

To overlay all three ECDFs on the same plot, you can use plt.plot() three times, once for each ECDF. Remember to include marker='.' and linestyle='none' as arguments inside plt.plot().

Instructions

- Compute ECDFs for each of the three species using your

ecdf()function. The variablessetosa_petal_length,versicolor_petal_length, andvirginica_petal_lengthare all in your namespace. Unpack the ECDFs intox_set,y_set,x_vers,y_versandx_virg,y_virg, respectively. - Plot all three ECDFs on the same plot as dots. To do this, you will need three

plt.plot()commands. Assign the result of each to_. - A legend and axis labels have been added for you, so hit ‘Submit Answer’ to see all the ECDFs!

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

virginica_petal_length = iris_df['petal length (cm)'][iris_df.species == 'virginica']

setosa_petal_length = iris_df['petal length (cm)'][iris_df.species == 'setosa']

# Compute ECDFs

x_set, y_set = ecdf(setosa_petal_length)

x_vers, y_vers = ecdf(versicolor_petal_length)

x_virg, y_virg = ecdf(virginica_petal_length)

# Plot all ECDFs on the same plot

plt.plot(x_set, y_set, marker='.', linestyle='none')

plt.plot(x_vers, y_vers, marker='.', linestyle='none')

plt.plot(x_virg, y_virg, marker='.', linestyle='none')

# Annotate the plot

plt.legend(('setosa', 'versicolor', 'virginica'), loc='lower right')

_ = plt.xlabel('petal length (cm)')

_ = plt.ylabel('ECDF')

# Display the plot

plt.show()

Onward toward the whole story

- Start with graphical eda!

Coming up…

- Thinking probabilistically

- Discrete and continuous distributions

- The power of hacker statistics using np.random()

Quantitative exploratory data analysis

In the last chapter, you learned how to graphically explore data. In this chapter, you will compute useful summary statistics, which serve to concisely describe salient features of a data set with a few numbers.

Introduction to summary statistics: The sample mean and median

- mean - average

- heavily influenced by outliers

np.mean()

- median - middle value of the sorted dataset

- immune to outlier influence

np.median()

Means and medians

Which one of the following statements is true about means and medians?

Possible Answers

An outlier can significantly affect the value of both the mean and the median.- An outlier can significantly affect the value of the mean, but not the median.

Means and medians are in general both robust to single outliers.The mean and median are equal if there is an odd number of data points.

Computing means

The mean of all measurements gives an indication of the typical magnitude of a measurement. It is computed using np.mean().

Instructions

- Compute the mean petal length of Iris versicolor from Anderson’s classic data set. The variable

versicolor_petal_lengthis provided in your namespace. Assign the mean tomean_length_vers.

1

2

3

4

5

# Compute the mean: mean_length_vers

mean_length_vers = np.mean(versicolor_petal_length)

# Print the result with some nice formatting

print('I. versicolor:', mean_length_vers, 'cm')

1

I. versicolor: 4.26 cm

with pandas.DataFrame

1

iris_df.groupby(['species']).mean()

| sepal length (cm) | sepal width (cm) | petal length (cm) | petal width (cm) | target | |

|---|---|---|---|---|---|

| species | |||||

| setosa | 5.006 | 3.428 | 1.462 | 0.246 | 0.0 |

| versicolour | 5.936 | 2.770 | 4.260 | 1.326 | 1.0 |

| virginica | 6.588 | 2.974 | 5.552 | 2.026 | 2.0 |

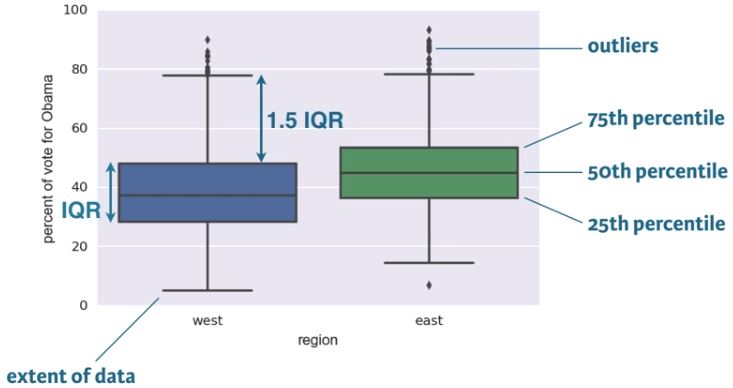

Percentiles, outliers and box plots

- The median is a special name for the 50th percentile

- 50% of the data are less than the median

- The 25th percentile is the value of the data point that is greater than 25% of the sorted data

- percentiles are useful summary statistics and can be computed using

np.percentile()

Computing Percentiles

1

np.percentile(df_swing['dem_share'], [25, 50, 75])

- Box plots are a graphical methode for displying summary statistics

- median is the middle line: 50th percentile

- bottom and top line of the box represent the 25th & 75th percentile, repectively

- the space between the 25th and 75th percentile is the interquartile range (IQR)

- Whiskers extent a distance of 1.5 time the IQR, or the extent of the data, whichever is less extreme

- Any points outside the whiskers are plotted as individual points, which we demarcate as outliers

- There is no single definition for an outlier, however, being more than 2 IQRs away from the median is a common criterion.

- An outlier is not necessarily erroneous

- Box plots are a great alternative to bee swarm plots, becasue bee swarm plots become too cluttered with large data sets

1

2

all_states = pd.read_csv(elections_all_file)

all_states.head()

| state | county | total_votes | dem_votes | rep_votes | other_votes | dem_share | east_west | |

|---|---|---|---|---|---|---|---|---|

| 0 | AK | State House District 8, Denali-University | 10320 | 4995 | 4983 | 342 | 50.06 | west |

| 1 | AK | State House District 37, Bristol Bay-Aleuti | 4665 | 1868 | 2661 | 136 | 41.24 | west |

| 2 | AK | State House District 12, Richardson-Glenn H | 7589 | 1914 | 5467 | 208 | 25.93 | west |

| 3 | AK | State House District 13, Greater Palmer | 11526 | 2800 | 8432 | 294 | 24.93 | west |

| 4 | AK | State House District 14, Greater Wasilla | 10456 | 2132 | 8108 | 216 | 20.82 | west |

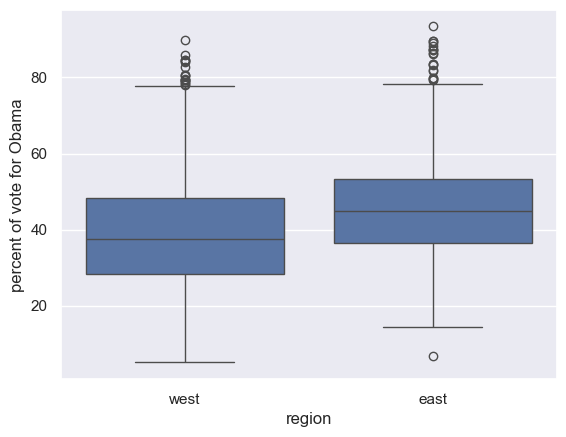

1

2

3

4

sns.boxplot(x='east_west', y='dem_share', data=all_states)

plt.xlabel('region')

plt.ylabel('percent of vote for Obama')

plt.show()

Computing percentiles

In this exercise, you will compute the percentiles of petal length of Iris versicolor.

Instructions

- Create

percentiles, a NumPy array of percentiles you want to compute. These are the 2.5th, 25th, 50th, 75th, and 97.5th. You can do so by creating a list containing these ints/floats and convert the list to a NumPy array usingnp.array(). For example,np.array([30, 50])would create an array consisting of the 30th and 50th percentiles. - Use

np.percentile()to compute the percentiles of the petal lengths from the Iris versicolor samples. The variableversicolor_petal_lengthis in your namespace.

1

2

3

4

5

6

7

8

# Specify array of percentiles: percentiles

percentiles = np.array([2.5, 25, 50, 75, 97.5])

# Compute percentiles: ptiles_vers

ptiles_vers = np.percentile(versicolor_petal_length, percentiles)

# Print the result

ptiles_vers

1

array([3.3 , 4. , 4.35 , 4.6 , 4.9775])

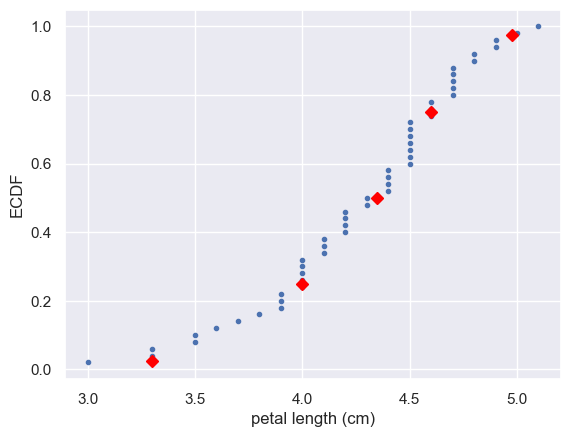

Comparing percentiles to ECDF

To see how the percentiles relate to the ECDF, you will plot the percentiles of Iris versicolor petal lengths you calculated in the last exercise on the ECDF plot you generated in chapter 1. The percentile variables from the previous exercise are available in the workspace as ptiles_vers and percentiles.

Note that to ensure the Y-axis of the ECDF plot remains between 0 and 1, you will need to rescale the percentiles array accordingly - in this case, dividing it by 100.

Instructions

- Plot the percentiles as red diamonds on the ECDF. Pass the x and y co-ordinates -

ptiles_versandpercentiles/100- as positional arguments and specify themarker='D',color='red'andlinestyle='none'keyword arguments. The argument for the y-axis -percentiles/100has been specified for you.

1

2

3

4

5

6

7

8

# Plot the ECDF

_ = plt.plot(x_vers, y_vers, '.')

_ = plt.xlabel('petal length (cm)')

_ = plt.ylabel('ECDF')

# Overlay percentiles as red diamonds.

_ = plt.plot(ptiles_vers, percentiles/100, marker='D', color='red', linestyle='none')

plt.show()

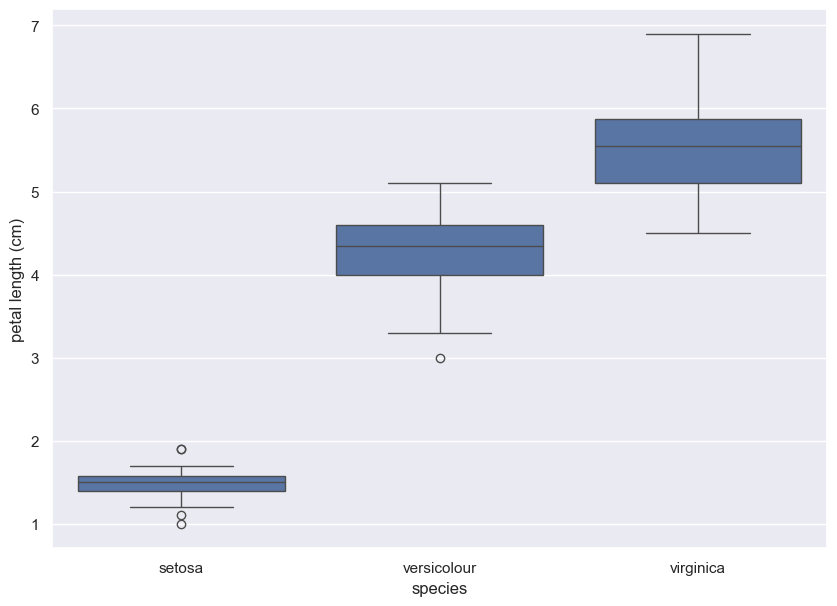

Box-and-whisker plot

Making a box plot for the petal lengths is unnecessary because the iris data set is not too large and the bee swarm plot works fine. However, it is always good to get some practice. Make a box plot of the iris petal lengths. You have a pandas DataFrame, df, which contains the petal length data, in your namespace. Inspect the data frame df in the IPython shell using df.head() to make sure you know what the pertinent columns are.

For your reference, the code used to produce the box plot in the video is provided below:

1

2

3

4

5

_ = sns.boxplot(x='east_west', y='dem_share', data=df_all_states)

_ = plt.xlabel('region')

_ = plt.ylabel('percent of vote for Obama')

In the IPython Shell, you can use sns.boxplot? or help(sns.boxplot) for more details on how to make box plots using seaborn.

Instructions

- The set-up is exactly the same as for the bee swarm plot; you just call

sns.boxplot()with the same keyword arguments as you wouldsns.swarmplot(). The x-axis is'species'and y-axis is'petal length (cm)'. - Don’t forget to label your axes!

1

2

3

4

5

6

7

8

9

10

fig, ax = plt.subplots(figsize=(10, 7))

# Create box plot with Seaborn's default settings

_ = sns.boxplot(x='species', y='petal length (cm)', data=iris_df)

# Label the axes

_ = plt.ylabel('petal length (cm)')

_ = plt.xlabel('species')

# Show the plot

plt.show()

Variance and standard deviation

- measures of spread

- variance:

- The mean squared distance of the data from the mean

- \[variance = \frac{1}{n}\sum_{i=1}^{n}(x_{i} - \overline{x})^2\]

- because of the squared quantity, variance doesn’t have the same units as the measurement

- standard deviation:

- \[\sqrt{variance}\]

Variance

1

dem_share_fl = all_states.dem_share[all_states.state == 'FL']

1

np.var(dem_share_fl)

1

147.44278618846067

1

2

all_states_var = all_states[['state', 'total_votes', 'dem_votes', 'rep_votes', 'other_votes', 'dem_share']].groupby(['state']).var(ddof=0)

all_states_var.dem_share.loc['FL']

1

147.44278618846067

1

all_states_var.head()

| total_votes | dem_votes | rep_votes | other_votes | dem_share | |

|---|---|---|---|---|---|

| state | |||||

| AK | 3.918599e+06 | 9.182529e+05 | 3.200012e+06 | 3.256997e+03 | 125.668270 |

| AL | 2.292250e+09 | 5.607371e+08 | 6.252062e+08 | 1.733390e+05 | 307.070511 |

| AR | 4.876461e+08 | 1.199459e+08 | 1.314874e+08 | 1.354781e+05 | 92.110499 |

| AZ | 1.135138e+11 | 2.266020e+10 | 3.343506e+10 | 1.616763e+07 | 114.874473 |

| CA | 2.349814e+11 | 1.040120e+11 | 2.620011e+10 | 9.319614e+07 | 177.821720 |

Standard Deviation

1

np.std(dem_share_fl)

1

12.142602117687158

1

np.sqrt(np.var(dem_share_fl))

1

12.142602117687158

1

2

all_states_std = all_states[['state', 'total_votes', 'dem_votes', 'rep_votes', 'other_votes', 'dem_share']].groupby(['state']).std(ddof=0)

all_states_std.dem_share.loc['FL']

1

12.142602117687158

1

all_states_std.head()

| total_votes | dem_votes | rep_votes | other_votes | dem_share | |

|---|---|---|---|---|---|

| state | |||||

| AK | 1979.545268 | 958.255147 | 1788.857869 | 57.070110 | 11.210186 |

| AL | 47877.444183 | 23679.887798 | 25004.123663 | 416.340031 | 17.523427 |

| AR | 22082.710391 | 10951.982529 | 11466.796262 | 368.073483 | 9.597421 |

| AZ | 336918.128317 | 150533.043458 | 182852.572197 | 4020.899516 | 10.717951 |

| CA | 484748.852298 | 322508.926289 | 161864.471516 | 9653.815033 | 13.334981 |

Computing the variance

It is important to have some understanding of what commonly-used functions are doing under the hood. Though you may already know how to compute variances, this is a beginner course that does not assume so. In this exercise, we will explicitly compute the variance of the petal length of Iris veriscolor using the equations discussed in the videos. We will then use np.var() to compute it.

Instructions

- Create an array called differences that is the

differencebetween the petal lengths (versicolor_petal_length) and the mean petal length. The variableversicolor_petal_lengthis already in your namespace as a NumPy array so you can take advantage of NumPy’s vectorized operations. - Square each element in this array. For example,

x**2squares each element in the arrayx. Store the result asdiff_sq. - Compute the mean of the elements in

diff_squsingnp.mean(). Store the result asvariance_explicit. - Compute the variance of

versicolor_petal_lengthusingnp.var(). Store the result asvariance_np. - Print both

variance_explicitandvariance_npin oneprintcall to make sure they are consistent.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

# Array of differences to mean: differences

differences = versicolor_petal_length - np.mean(versicolor_petal_length)

# Square the differences: diff_sq

diff_sq = differences**2

# Compute the mean square difference: variance_explicit

variance_explicit = np.mean(diff_sq)

# Compute the variance using NumPy: variance_np

variance_np = np.var(versicolor_petal_length)

# Print the results

print(variance_explicit, variance_np)

1

0.21640000000000004 0.21640000000000004

The standard deviation and the variance

As mentioned in the video, the standard deviation is the square root of the variance. You will see this for yourself by computing the standard deviation using np.std() and comparing it to what you get by computing the variance with np.var() and then computing the square root.

Instructions

- Compute the variance of the data in the

versicolor_petal_lengtharray usingnp.var()and store it in a variable calledvariance. - Print the square root of this value.

- Print the standard deviation of the data in the

versicolor_petal_lengtharray usingnp.std()

1

2

3

4

5

6

7

8

9

10

# Compute the variance: variance

variance = np.var(versicolor_petal_length)

# Print the square root of the variance

std_explicit = np.sqrt(variance)

# Print the standard deviation

std_np = np.std(versicolor_petal_length)

print(std_explicit, std_np)

1

0.4651881339845203 0.4651881339845203

Covariance and Pearson correlation coefficient

- Covariance

- \[covariance = \frac{1}{n}\sum_{i=1}^{n}(x_{i} - \overline{x})(y_{i} - \overline{y})\]

- The data point differs from the mean vote share and the mean total votes for Obama

- The differences for each data point can be computed

- The covariance is the mean of the product of these differences

- If both x and y tend to be above or below their respective means together, as they are in this data set, the covariance is positive.

- This means they are positively correlated:

- When x is high, so is y

- When the county is populous, it has more votes for Obama

- This means they are positively correlated:

- If x is high while y is low, the covariance is negative

- This means they are negatively correlated (anticorrelated) - not the case for this data set.

- Pearson correlation

- A more generally applicable measure of how two variables depend on each other, should be dimensionless (not units).

- \[\rho = Pearson\space correlation = \frac{covariance}{(std\space of\space x)(std\space of\space y)}\]

- \[\rho = \frac{variability\space due\space to\space codependence}{independent\space variability}\]

- Comparison of the variability in the data due to codependence (the covariance) to the variability inherent to each variable independently (their standard deviations).

- It’s dimensionless and ranges from -1 (for complete anticorrelation) to 1 (for complete correlation).

- A value of zero means there is no correlation between the data, as shown in the upper left plot.

- Good metric for correlation between two variables.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

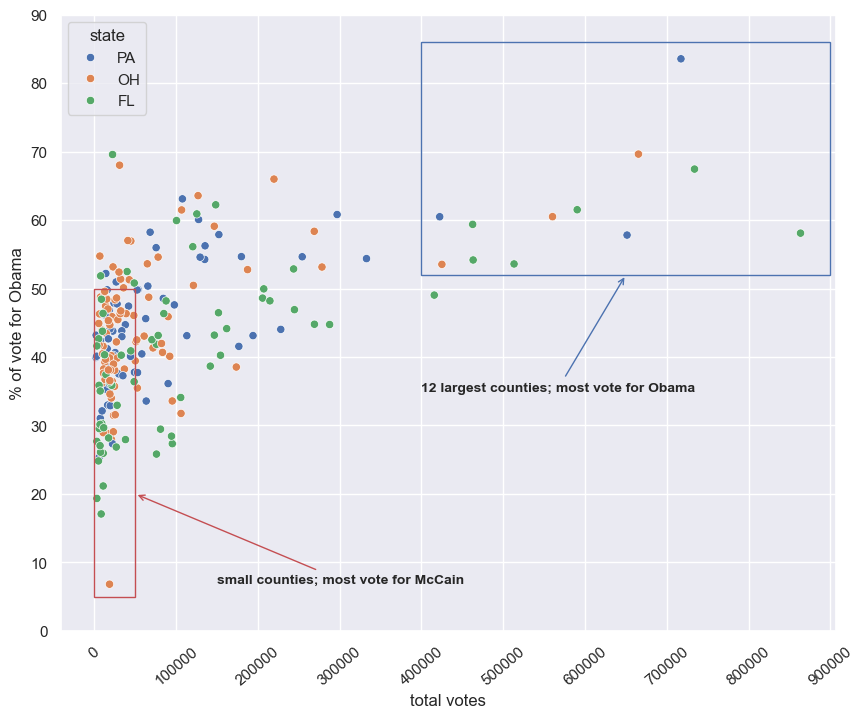

plt.figure(figsize=(10, 8))

sns.scatterplot(x='total_votes', y='dem_share', data=swing, hue='state')

plt.xlabel('total votes')

plt.ylabel('% of vote for Obama')

plt.xticks([x for x in range(0, 1000000, 100000)], rotation=40)

plt.yticks([x for x in range(0, 100, 10)])

# Create a Rectangle patch

plt.gca().add_patch(Rectangle((400000, 52), 500000, 34, linewidth=1, edgecolor='b', facecolor='none'))

plt.gca().add_patch(Rectangle((0, 5), 50000, 45, linewidth=1, edgecolor='r', facecolor='none'))

# Annotate

plt.annotate('12 largest counties; most vote for Obama', xy=(650000, 52), weight='bold',

xytext=(400000, 35), fontsize=10, arrowprops=dict(arrowstyle="->", color='b'))

plt.annotate('small counties; most vote for McCain', xy=(50000, 20), weight='bold',

xytext=(150000, 7), fontsize=10, arrowprops=dict(arrowstyle="->", color='r'))

plt.show()

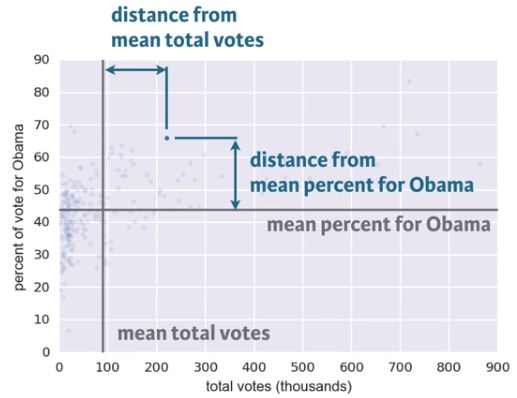

Scatter plots

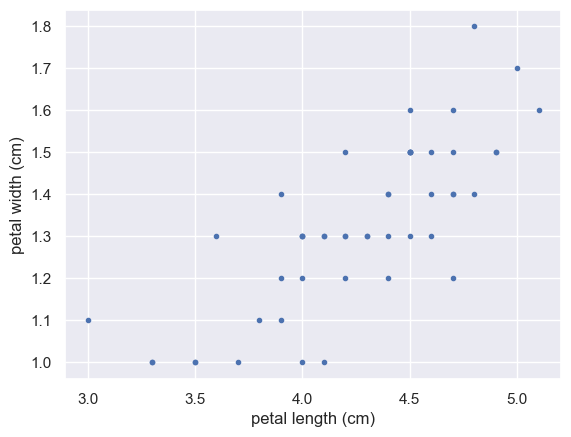

When you made bee swarm plots, box plots, and ECDF plots in previous exercises, you compared the petal lengths of different species of iris. But what if you want to compare two properties of a single species? This is exactly what we will do in this exercise. We will make a scatter plot of the petal length and width measurements of Anderson’s Iris versicolor flowers. If the flower scales (that is, it preserves its proportion as it grows), we would expect the length and width to be correlated.

For your reference, the code used to produce the scatter plot in the video is provided below:

1

2

3

_ = plt.plot(total_votes/1000, dem_share, marker='.', linestyle='none')

_ = plt.xlabel('total votes (thousands)')

_ = plt.ylabel('percent of vote for Obama')

Instructions

- Use

plt.plot()with the appropriate keyword arguments to make a scatter plot of versicolor petal length (x-axis) versus petal width (y-axis). The variablesversicolor_petal_lengthandversicolor_petal_widthare already in your namespace. Do not forget to use themarker='.'andlinestyle='none'keyword arguments. - Label the axes.

- Display the plot.

1

2

3

4

5

6

7

8

9

10

11

versicolor_petal_width = iris_df['petal width (cm)'][iris_df.species == 'versicolour']

# Make a scatter plot

_ = plt.plot(versicolor_petal_length, versicolor_petal_width, marker='.', linestyle='none')

# Label the axes

_ = plt.xlabel('petal length (cm)')

_ = plt.ylabel('petal width (cm)')

# Show the result

plt.show()

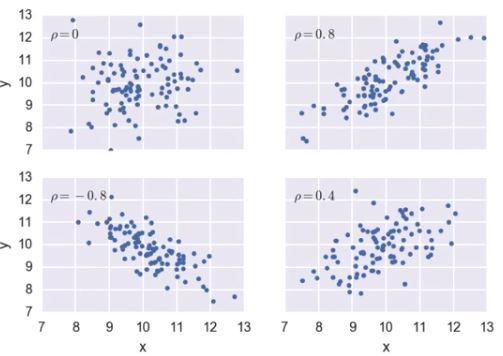

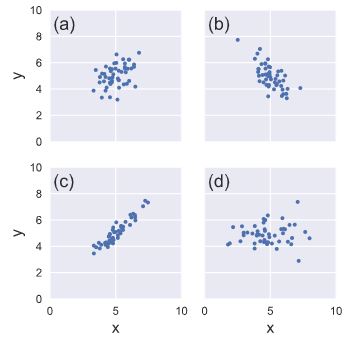

Variance and covariance by looking

Consider four scatter plots of x-y data, appearing to the right. Which has, respectively,

- the highest variance in the variable x,

- the highest covariance,

- negative covariance?

Instructions

Possible Answers

a, c, bd, c, a- **d, c, b**

d, d, b

Computing the covariance

The covariance may be computed using the Numpy function np.cov(). For example, we have two sets of data x and y, np.cov(x, y) returns a 2D array where entries [0,1] and [1,0] are the covariances. Entry [0,0] is the variance of the data in x, and entry [1,1] is the variance of the data in y. This 2D output array is called the covariance matrix, since it organizes the self- and covariance.

To remind you how the I. versicolor petal length and width are related, we include the scatter plot you generated in a previous exercise.

Instructions

- Use

np.cov()to compute the covariance matrix for the petal length (versicolor_petal_length) and width (versicolor_petal_width) of I. versicolor. - Print the covariance matrix.

- Extract the covariance from entry

[0,1]of the covariance matrix. Note that by symmetry, entry[1,0]is the same as entry[0,1]. - Print the covariance.

1

iris_df[['petal length (cm)', 'petal width (cm)']][iris_df.species == 'versicolour'].cov()

| petal length (cm) | petal width (cm) | |

|---|---|---|

| petal length (cm) | 0.220816 | 0.073102 |

| petal width (cm) | 0.073102 | 0.039106 |

1

2

3

4

5

# Compute the covariance matrix: covariance_matrix

covariance_matrix = np.cov(versicolor_petal_length, versicolor_petal_width)

# Print covariance matrix

covariance_matrix

1

2

array([[0.22081633, 0.07310204],

[0.07310204, 0.03910612]])

1

2

3

4

5

# Extract covariance of length and width of petals: petal_cov

petal_cov = covariance_matrix[0, 1]

# Print the length/width covariance

petal_cov

1

0.07310204081632653

Computing the Pearson correlation coefficient

As mentioned in the video, the Pearson correlation coefficient, also called the Pearson r, is often easier to interpret than the covariance. It is computed using the np.corrcoef() function. Like np.cov(), it takes two arrays as arguments and returns a 2D array. Entries [0,0] and [1,1] are necessarily equal to 1 (can you think about why?), and the value we are after is entry [0,1].

In this exercise, you will write a function, pearson_r(x, y) that takes in two arrays and returns the Pearson correlation coefficient. You will then use this function to compute it for the petal lengths and widths of I. versicolor.

Again, we include the scatter plot you generated in a previous exercise to remind you how the petal width and length are related.

Instructions

- Define a function with signature

pearson_r(x, y).- Use

np.corrcoef()to compute the correlation matrix ofxandy(pass them tonp.corrcoef()in that order). - The function returns entry

[0,1]of the correlation matrix.

- Use

- Compute the Pearson correlation between the data in the arrays

versicolor_petal_lengthandversicolor_petal_width. Assign the result tor. - Print the result.

1

iris_df[['petal length (cm)', 'petal width (cm)']][iris_df.species == 'versicolour'].corr()

| petal length (cm) | petal width (cm) | |

|---|---|---|

| petal length (cm) | 1.000000 | 0.786668 |

| petal width (cm) | 0.786668 | 1.000000 |

1

2

3

4

5

6

7

8

9

10

11

12

13

def pearson_r(x, y):

"""Compute Pearson correlation coefficient between two arrays."""

# Compute correlation matrix: corr_mat

corr_mat = np.corrcoef(x, y)

# Return entry [0,1]

return corr_mat[0,1]

# Compute Pearson correlation coefficient for I. versicolor: r

r = pearson_r(versicolor_petal_length, versicolor_petal_width)

# Print the result

print(r)

1

0.7866680885228169

Thinking probabilistically: Discrete variables

Statistical inference rests upon probability. Because we can very rarely say anything meaningful with absolute certainty from data, we use probabilistic language to make quantitative statements about data. In this chapter, you will learn how to think probabilistically about discrete quantities, those that can only take certain values, like integers. It is an important first step in building the probabilistic language necessary to think statistically.

Probabilistic logic and statistical inference

- Probabilistic reasoning allows us to describe uncertainty

- Given a set of data, you describe probabilistically what you might expect if those data were acquired repeatedly

- This is the heart of statistical inference

- It’s the process by which we go from measured data to probabilistic conclusions about what we might expect if we collected the same data again.

What is the goal of statistical inference?

Why do we do statistical inference?

Possible Answers

- To draw probabilistic conclusions about what we might expect if we collected the same data again.

- To draw actionable conclusions from data.

- To draw more general conclusions from relatively few data or observations.

- **All of these.**

Why do we use the language of probablility?

Which of the following is not a reason why we use probabilistic language in statistical inference?

Possible Answers

- Probability provides a measure of uncertainty.

- **Probabilistic language is not very precise.**

- Data are almost never exactly the same when acquired again, and probability allows us to say how much we expect them to vary.

Random number generators and hacker statistics

- Instead o repeating data acquisition over and over, repeated measurements can be simulated

- The concepts of probabilities originated from games of chance

- What’s the probability of getting 4 heads with 4 flips of a coin?

- This type of data can be generated using

np.random.random- drawn a number between 0 and 1

- $<0.5\longrightarrow\text{heads}$

- $\geq0.5\longrightarrow\text{tails}$

- The pseudo random number generator works by starting with an integer, called a seed, and then generates random numbers in succession

- The same seed gives the same sequence of random numbers

- Manually seed the random number generator for reproducible results

- Specified using

np.random.seed()

Bernoulli Trial

- An experiment that has two options, “success” (True) and “failure” (False).

Hacker stats probabilities

- Determine how to simulate data

- Simulated it repeatedly

- Compute the fraction of trials that had the outcome of interest

- Probability is approximately the fraction of trials with the outcome of interest

Simulated coin flips

1

2

3

4

np.random.seed(42)

random_numbers = np.random.random(size=4)

random_numbers

1

array([0.37454012, 0.95071431, 0.73199394, 0.59865848])

1

2

3

heads = random_numbers < 0.5

heads

1

array([ True, False, False, False])

1

np.sum(heads)

1

1

- The number of heads can be computed by summing the array of Booleans, because in numerical contexts, Python treats True as 1 and False as 0.

We want to know the probability of getting four heads if we were to repeatedly flip the 4 coins

- without

list comprehension

1

2

3

4

5

6

7

n_all_heads = 0 # initialize number of 4-heads trials

for _ in range(10000):

heads = np.random.random(size=4) < 0.5

n_heads = np.sum(heads)

if n_heads == 4:

n_all_heads += 1

- with

list comprehension

1

n_all_heads = sum([1 for _ in range(10000) if sum(np.random.random(size=4) < 0.5) == 4])

1

n_all_heads

1

619

1

n_all_heads/10000

1

0.0619

Generating random numbers using the np.random module

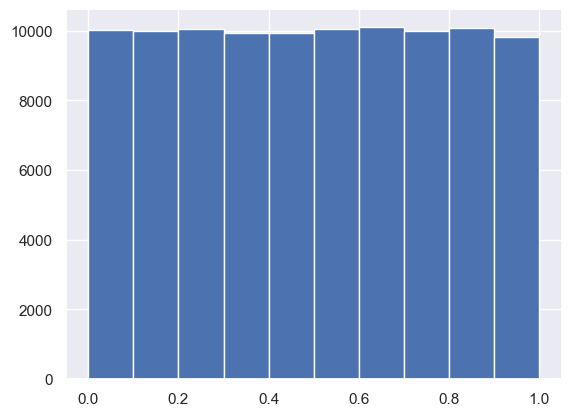

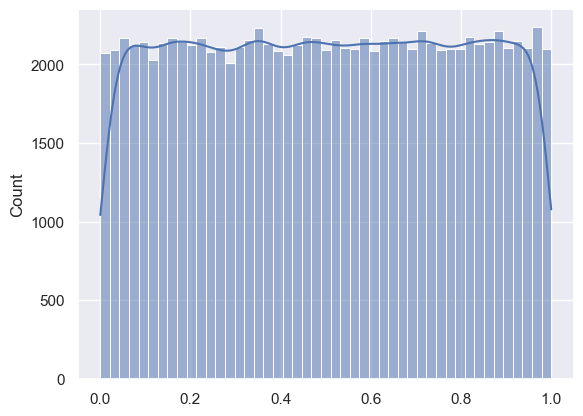

We will be hammering the np.random module for the rest of this course and its sequel. Actually, you will probably call functions from this module more than any other while wearing your hacker statistician hat. Let’s start by taking its simplest function, np.random.random() for a test spin. The function returns a random number between zero and one. Call np.random.random() a few times in the IPython shell. You should see numbers jumping around between zero and one.

In this exercise, we’ll generate lots of random numbers between zero and one, and then plot a histogram of the results. If the numbers are truly random, all bars in the histogram should be of (close to) equal height.

You may have noticed that, in the video, Justin generated 4 random numbers by passing the keyword argument size=4 to np.random.random(). Such an approach is more efficient than a for loop: in this exercise, however, you will write a for loop to experience hacker statistics as the practice of repeating an experiment over and over again.

Instructions

- Seed the random number generator using the seed

42. - Initialize an empty array,

random_numbers, of 100,000 entries to store the random numbers. Make sure you usenp.empty(100000)to do this. - Write a

forloop to draw 100,000 random numbers usingnp.random.random(), storing them in therandom_numbersarray. To do so, loop overrange(100000). - Plot a histogram of

random_numbers. It is not necessary to label the axes in this case because we are just checking the random number generator. Hit ‘Submit Answer’ to show your plot.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

# Seed the random number generator

np.random.seed(42)

# Initialize random numbers: random_numbers

random_numbers = np.empty(100000)

# Generate random numbers by looping over range(100000)

for i in range(100000):

random_numbers[i] = np.random.random()

# Plot a histogram

_ = plt.hist(random_numbers)

# Show the plot

plt.show()

1

2

sns.histplot(random_numbers, kde=True)

plt.show()

The histogram is nearly flat across the top, indicating there is equal chance a randomly-generated number is in any of the histogram bins.

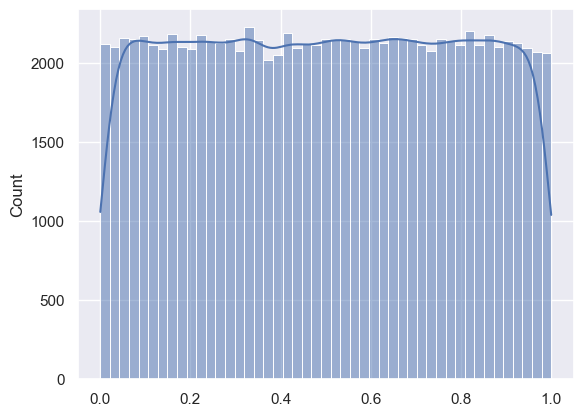

Using np.random.rand

1

rand_num = np.random.rand(100000)

1

2

sns.histplot(rand_num, kde=True)

plt.show()

The np.random module and Bernoulli trials

You can think of a Bernoulli trial as a flip of a possibly biased coin. Specifically, each coin flip has a probability p of landing heads (success) and probability 1−p of landing tails (failure). In this exercise, you will write a function to perform n Bernoulli trials, perform_bernoulli_trials(n, p), which returns the number of successes out of n Bernoulli trials, each of which has probability p of success. To perform each Bernoulli trial, use the np.random.random() function, which returns a random number between zero and one.

Instructions

- Define a function with signature

perform_bernoulli_trials(n, p).- Initialize to zero a variable

n_successthe counter ofTrueoccurrences, which are Bernoulli trial successes. - Write a

forloop where you perform a Bernoulli trial in each iteration and increment the number of success if the result isTrue. Performniterations by looping overrange(n).- To perform a Bernoulli trial, choose a random number between zero and one using

np.random.random(). If the number you chose is less thanp, increment n_success (use the+= 1operator to achieve this).

- To perform a Bernoulli trial, choose a random number between zero and one using

- Initialize to zero a variable

- The function returns the number of successes

n_success.

def perform_bernoulli_trials()

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

def perform_bernoulli_trials(n: int=100000, p: float=0.5) -> int:

"""

Perform n Bernoulli trials with success probability p

and return number of successes.

n: number of iterations

p: target number between 0 and 1, inclusive

"""

# Initialize number of successes: n_success

n_success = 0

# Perform trials

for i in range(n):

# Choose random number between zero and one: random_number

random_number = np.random.random()

# If less than p, it's a success so add one to n_success

if random_number < p:

n_success += 1

return n_success

With list comprehension

1

2

3

4

5

6

7

8

9

def perform_bernoulli_trials(n: int=100000, p: float=0.5) -> int:

"""

Perform n Bernoulli trials with success probability p

and return number of successes.

n: number of iterations

p: target number between 0 and 1, inclusive

"""

return sum([1 for _ in range(n) if np.random.random() < p])

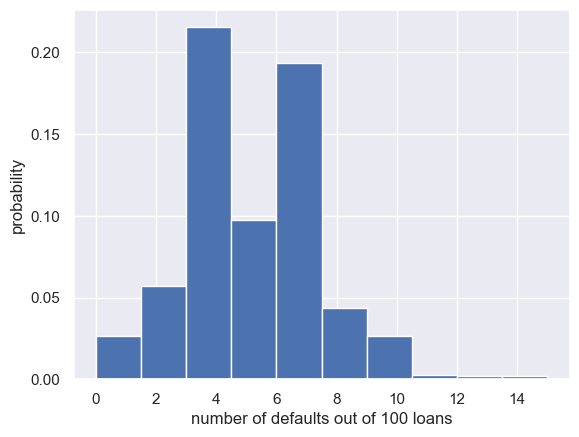

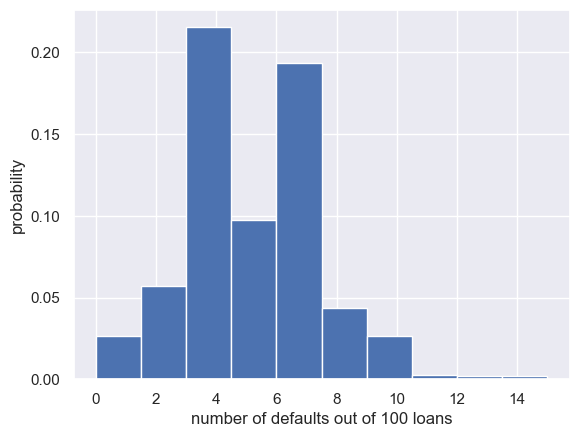

How many defaults might we expect?

Let’s say a bank made 100 mortgage loans. It is possible that anywhere between 0 and 100 of the loans will be defaulted upon. You would like to know the probability of getting a given number of defaults, given that the probability of a default is p = 0.05. To investigate this, you will do a simulation. You will perform 100 Bernoulli trials using the perform_bernoulli_trials() function you wrote in the previous exercise and record how many defaults we get. Here, a success is a default. (Remember that the word “success” just means that the Bernoulli trial evaluates to True, i.e., did the loan recipient default?) You will do this for another 100 Bernoulli trials. And again and again until we have tried it 1000 times. Then, you will plot a histogram describing the probability of the number of defaults.

Instructions

- Seed the random number generator to 42.

- Initialize

n_defaults, an empty array, usingnp.empty(). It should contain 1000 entries, since we are doing 1000 simulations. - Write a

forloop with1000iterations to compute the number of defaults per 100 loans using theperform_bernoulli_trials()function. It accepts two arguments: the number of trialsn- in this case 100 - and the probability of successp- in this case the probability of a default, which is0.05. On each iteration of the loop store the result in an entry ofn_defaults. - Plot a histogram of

n_defaults. Include thenormed=Truekeyword argument so that the height of the bars of the histogram indicate the probability.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

# Seed random number generator

np.random.seed(42)

# Initialize the number of defaults: n_defaults

n_defaults = np.empty(1000)

# Compute the number of defaults

for i in range(1000):

n_defaults[i] = perform_bernoulli_trials(100, 0.05)

# Plot the histogram with default number of bins; label your axes

_ = plt.hist(n_defaults, density=True)

_ = plt.xlabel('number of defaults out of 100 loans')

_ = plt.ylabel('probability')

# Show the plot

plt.show()

This is not an optimal way to plot a histogram when the results are known to be integers. This will be revisited in forthcoming exercises.

With list comprehension

1

2

3

4

5

6

7

np.random.seed(42)

n_defaults = np.asarray([perform_bernoulli_trials(100, 0.05) for _ in range(1000)])

plt.hist(n_defaults, density=True)

plt.xlabel('number of defaults out of 100 loans')

plt.ylabel('probability')

plt.show()

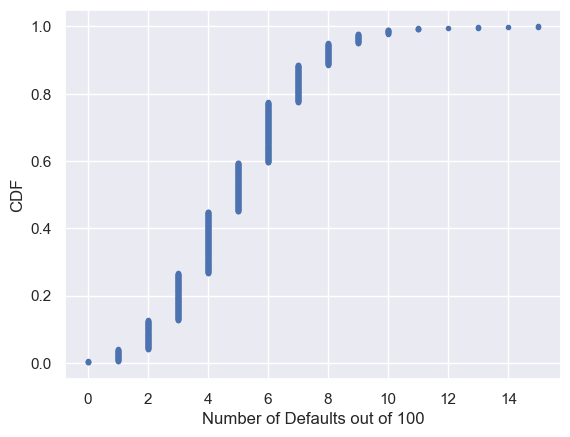

Will the bank fail?

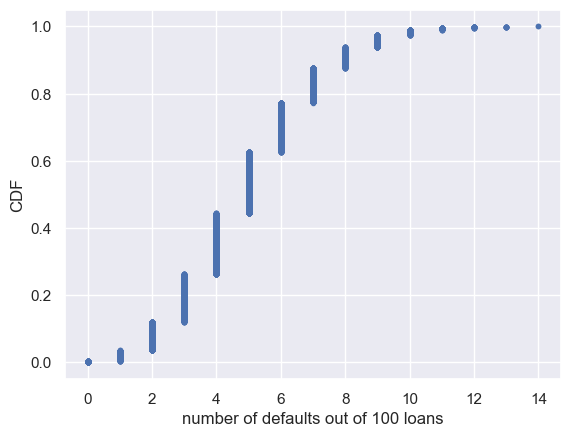

Using def ecdf() from the first section, plot the number of n_defaults from the previous exercise, as a CDF.

If interest rates are such that the bank will lose money if 10 or more of its loans are defaulted upon, what is the probability that the bank will lose money?

Instructions

- Compute the

xandyvalues for the ECDF ofn_defaults. - Plot the ECDF, making sure to label the axes. Remember to include

marker='.'andlinestyle='none'in addition toxandyin your callplt.plot(). - Show the plot.

- Compute the total number of entries in your

n_defaultsarray that were greater than or equal to 10. To do so, compute a boolean array that tells you whether a given entry ofn_defaultsis>= 10. Then sum all the entries in this array usingnp.sum(). For example,np.sum(n_defaults <= 5)would compute the number of defaults with 5 or fewer defaults. - The probability that the bank loses money is the fraction of

n_defaultsthat are greater than or equal to 10.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

# Compute ECDF: x, y

x, y = ecdf(n_defaults)

# Plot the ECDF with labeled axes

plt.plot(x, y, marker='.', linestyle='none')

plt.xlabel('Number of Defaults out of 100')

plt.ylabel('CDF')

# Show the plot

plt.show()

# Compute the number of 100-loan simulations with 10 or more defaults: n_lose_money

n_lose_money = sum(n_defaults >= 10)

# Compute and print probability of losing money

print('Probability of losing money =', n_lose_money / len(n_defaults))

1

Probability of losing money = 0.022

As might be expected, about 5/100 defaults occur. There’s about a 2% chance of getting 10 or more defaults out of 100 loans.

Probability distributions and stories: The Binomial distribution

Probability Mass Function (PMF)

- Probability mass function

- The set of probabilities of discrete outcomes

- PMF is a property of a discrete probability distribution

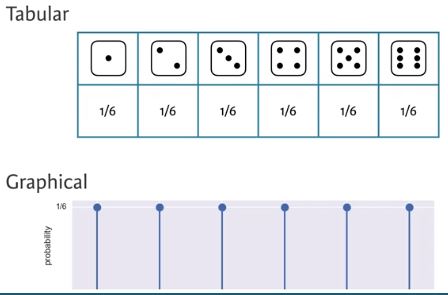

Discrete Uniform PMF

- The outcomes are discrete because only certain values may be attained; there is not option for 3.7

- Each result has a uniform probability of 1/6

Probability Distribution

- Probability distribution

- A mathematical description of outcomes

Discrete Uniform Distribution

- Discrete uniform distribution

- The outcome of rolling a single fair die, is Discrete Uniformly distributed

Binomial Distribution

- Binomial distribution

- The number r of successes in n Bernoulli trials with probability p of success, is Binomially distributed

- The number r of heads in 4 coin flips with probability p = 0.5 of heads, is Binomially distributed

1

np.random.binomial(4, 0.5)

1

2

1

np.random.binomial(4, 0.5, size=10)

1

array([2, 2, 2, 2, 2, 3, 3, 2, 2, 0])

Binomial PMF

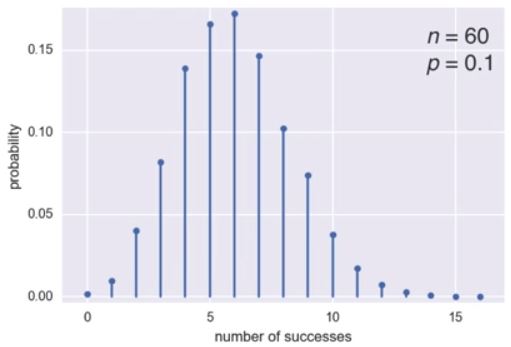

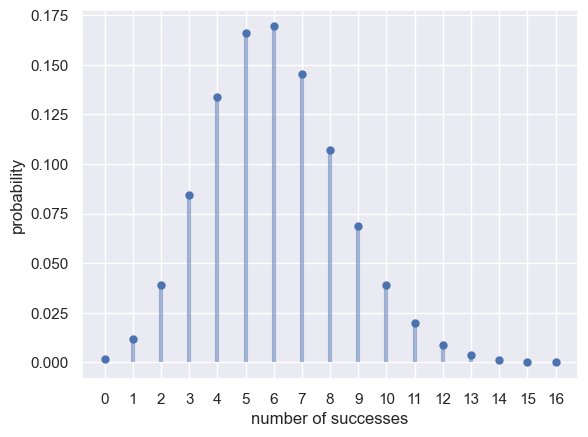

- To plot the Binomial PMF, take 10000 samples from a Binomial distribution of 60 Bernoulli trials with a probability of success of 0.1

- The most likely number of successes is 6 out of 60, but it’s possible to get as many as 11 or as few as 1

scipy.stats.binom

1

2

3

np.random.seed(42)

samples = np.random.binomial(60, 0.1, size=10_000)

samples

1

array([ 5, 10, 7, ..., 10, 5, 4])

1

2

3

4

5

6

7

8

9

10

n, p = 60, 0.1

x = [x for x in range(17)]

fig, ax = plt.subplots(1, 1)

ax.plot(x, binom.pmf(x, n, p), 'bo', ms=5, label='binom pmf')

ax.vlines(x, 0, binom.pmf(x, n, p), colors='b', lw=3, alpha=0.5)

plt.xticks(x)

plt.ylabel('probability')

plt.xlabel('number of successes')

plt.show()

1

2

3

4

5

6

7

8

sns.set()

x, y = ecdf(samples)

plt.plot(x, y, marker='.', linestyle='none')

plt.margins(0.02)

plt.xlabel('Number of Successes')

plt.ylabel('CDF')

plt.show()

Sampling out of the Binomial distribution

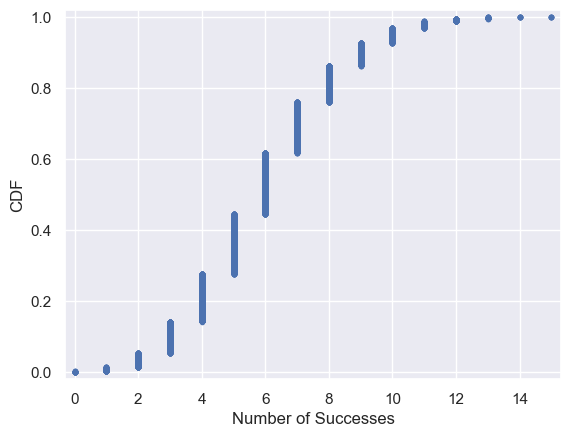

Compute the probability mass function for the number of defaults we would expect for 100 loans as in the last section, but instead of simulating all of the Bernoulli trials, perform the sampling using np.random.binomial(). This is identical to the calculation you did in the last set of exercises using your custom-written perform_bernoulli_trials() function, but far more computationally efficient. Given this extra efficiency, we will take 10,000 samples instead of 1000. After taking the samples, plot the CDF as last time. This CDF that you are plotting is that of the Binomial distribution.

Note: For this exercise and all going forward, the random number generator is pre-seeded for you (with np.random.seed(42)) to save you typing that each time.

Instructions

- Draw samples out of the Binomial distribution using

np.random.binomial(). You should use parametersn = 100andp = 0.05, and set thesize = 10000. - Compute the CDF using your previously-written

ecdf()function. - Plot the CDF with axis labels. The x-axis here is the number of defaults out of 100 loans, while the y-axis is the CDF.

1

2

3

4

5

6

7

8

9

10

11

12

# Take 10,000 samples out of the binomial distribution: n_defaults

np.random.seed(42)

n_defaults = np.random.binomial(100, 0.05, size=10_000)

# Compute CDF: x, y

x, y = ecdf(n_defaults)

# Plot the CDF with axis labels

plt.plot(x, y, marker='.', linestyle='none')

plt.xlabel('number of defaults out of 100 loans')

plt.ylabel('CDF')

plt.show()

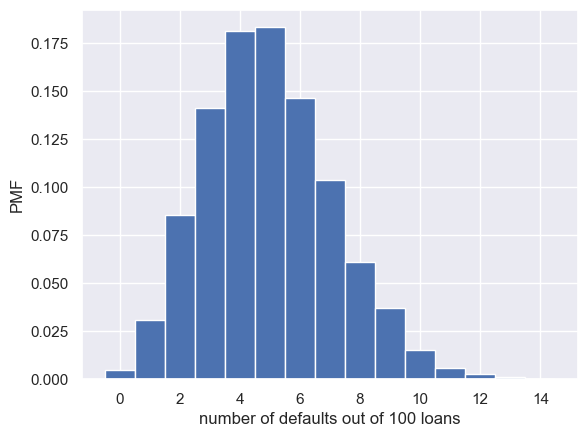

Plotting the Binomial PMF

As mentioned in the video, plotting a nice looking PMF requires a bit of matplotlib trickery that we will not go into here. Instead, we will plot the PMF of the Binomial distribution as a histogram with skills you have already learned. The trick is setting up the edges of the bins to pass to plt.hist() via the bins keyword argument. We want the bins centered on the integers. So, the edges of the bins should be -0.5, 0.5, 1.5, 2.5, ... up to max(n_defaults) + 1.5. You can generate an array like this using np.arange() and then subtracting 0.5 from the array.

You have already sampled out of the Binomial distribution during your exercises on loan defaults, and the resulting samples are in the NumPy array n_defaults.

Instructions

- Using

np.arange(), compute the bin edges such that the bins are centered on the integers. Store the resulting array in the variablebins. - Use

plt.hist()to plot the histogram ofn_defaultswith thenormed=Trueandbins=binskeyword arguments.

1

2

3

4

5

6

7

8

9

10

11

12

# Compute bin edges: bins

bins = np.arange(0, max(n_defaults) + 1.5) - 0.5

# Generate histogram

plt.hist(n_defaults, density=True, bins=bins)

# Label axes

plt.xlabel('number of defaults out of 100 loans')

plt.ylabel('PMF')

# Show the plot

plt.show()

Poisson processes and the Poisson distribution

- Poisson distribution

- The timing of the next event is completely independent of when the previous event occurred

- Examples of Poisson processes:

- Natural births in a given hospital

- There is a well-defined average number of natural births per year, and the timing of one birth is independent of the timing of the previous one

- Hits on a website during a given hour

- The timing of successive hits is independent of the timing of the previous hit

- Meteor strikes

- Molecular collisions in a gas

- Aviation incidents

- Natural births in a given hospital

- The number of arrivals of a Poisson process in a given amount of time is Poisson distributed

- The number of arrivals r of a Poisson process in a given time interval with average rate of arrivals $\lambda$ per interval is Poisson distributed

- The Poisson distribution has one parameter, the average number of arrivals in a given length of time

- The number of hits r on a website in one hour with an average hit rate of 6 hits per hour is Poisson distributed

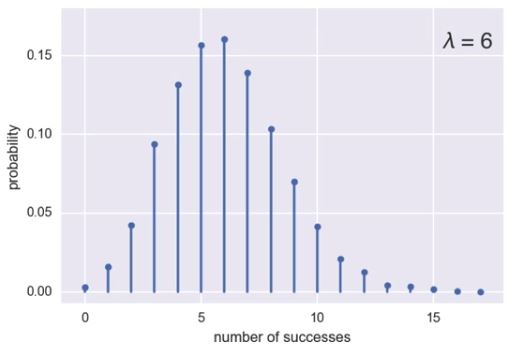

Poisson PMF

- For the preceding plot, for a given hour, the site is likely to get 6 hits, which is the average, but it’s possible to also get 10, or none

- This looks like the Binomial PMF from 3.3.0.5.1. Binomial PMF The Poisson distribution is a limit of the Binomial distribution for low probability of success and large number of trials, i.e. for rare events

- To sample from the Poisson distribution, use

np.random.poisson.- It also has the size keyword argument to allow multiple samples

- The Poisson CDF resembles the Binomial CDF

Poisson CDF

1

2

3

4

5

6

7

8

samples = np.random.poisson(6, size=10_000)

x, y = ecdf(samples)

plt.plot(x, y, marker='.', linestyle='none')

plt.margins(0.02)

plt.xlabel('number of successes')

plt.ylabel('CDF')

plt.show()

Relationship between Binomial and Poisson distribution

You just heard that the Poisson distribution is a limit of the Binomial distribution for rare events. This makes sense if you think about the stories. Say we do a Bernoulli trial every minute for an hour, each with a success probability of 0.1. We would do 60 trials, and the number of successes is Binomially distributed, and we would expect to get about 6 successes. This is just like the Poisson story we discussed in the video, where we get on average 6 hits on a website per hour. So, the Poisson distribution with arrival rate equal to np approximates a Binomial distribution for n Bernoulli trials with probability p of success (with n large and p small). Importantly, the Poisson distribution is often simpler to work with because it has only one parameter instead of two for the Binomial distribution.

Let’s explore these two distributions computationally. You will compute the mean and standard deviation of samples from a Poisson distribution with an arrival rate of 10. Then, you will compute the mean and standard deviation of samples from a Binomial distribution with parameters n and p such that np=10.

Instructions

- Using the

np.random.poisson()function, draw10000samples from a Poisson distribution with a mean of10. - Make a list of the

nandpvalues to consider for the Binomial distribution. Choosen = [20, 100, 1000]andp = [0.5, 0.1, 0.01]so that np is always 10. - Using

np.random.binomial()inside the providedforloop, draw10000samples from a Binomial distribution with eachn, ppair and print the mean and standard deviation of the samples. There are 3n, ppairs:20, 0.5,100, 0.1, and1000, 0.01. These can be accessed inside the loop asn[i], p[i].

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

# Draw 10,000 samples out of Poisson distribution: samples_poisson

samples_poisson = np.random.poisson(10, size=10_000)

# Print the mean and standard deviation

print(f'Poisson: Mean = {np.mean(samples_poisson)} Std = {np.std(samples_poisson):0.03f}')

# Specify values of n and p to consider for Binomial: n, p

n = [20, 100, 1_000, 10_000]

p = [0.5, 0.1, 0.01, 0.001]

# Draw 10,000 samples for each n,p pair: samples_binomial

for i in range(4):

samples_binomial = np.random.binomial(n[i], p[i], size=10_000)

# Print results

print(f'n = {n[i]} Binom: Mean = {np.mean(samples_binomial)} Std = {np.std(samples_binomial):0.03f}')

1

2

3

4

5

Poisson: Mean = 10.0421 Std = 3.172

n = 20 Binom: Mean = 10.0064 Std = 2.248

n = 100 Binom: Mean = 9.9371 Std = 2.980

n = 1000 Binom: Mean = 10.0357 Std = 3.164

n = 10000 Binom: Mean = 10.0881 Std = 3.195

The means are all about the same. The standard deviation of the Binomial distribution gets closer and closer to that of the Poisson distribution as the probability p gets lower and lower.

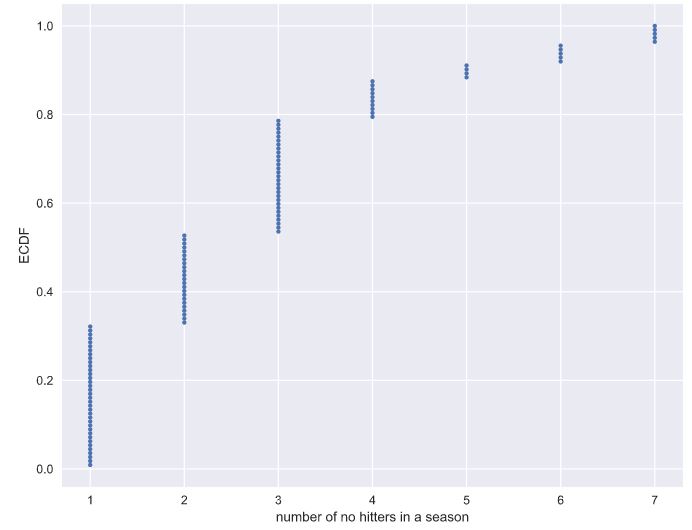

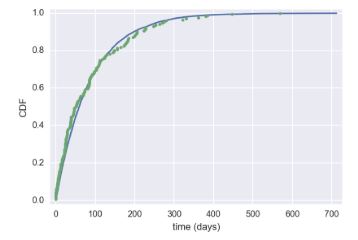

How many no-hitters in a season?

In baseball, a no-hitter is a game in which a pitcher does not allow the other team to get a hit. This is a rare event, and since the beginning of the so-called modern era of baseball (starting in 1901), there have only been 251 of them through the 2015 season in over 200,000 games. The ECDF of the number of no-hitters in a season is shown to the right. Which probability distribution would be appropriate to describe the number of no-hitters we would expect in a given season?

Note: The no-hitter data set was scraped and calculated from the data sets available at retrosheet.org (license).

Possible Answers

Discrete uniformBinomialPoisson- **Both Binomial and Poisson, though Poisson is easier to model and compute.**

Both Binomial and Poisson, though Binomial is easier to model and compute.

With rare events (low p, high n), the Binomial distribution is Poisson. This has a single parameter, the mean number of successes per time interval, in this case the mean number of no-hitters per season.

Was 2015 anomalous?

1990 and 2015 featured the most no-hitters of any season of baseball (there were seven). Given that there are on average 251/115 no-hitters per season, what is the probability of having seven or more in a season?

Instructions

- Draw

10000samples from a Poisson distribution with a mean of251/115and assign ton_nohitters. - Determine how many of your samples had a result greater than or equal to

7and assign ton_large. - Compute the probability,

p_large, of having7or more no-hitters by dividingn_largeby the total number of samples (10000). - Hit ‘Submit Answer’ to print the probability that you calculated.

1

2

3

4

5

6

7

8

9

10

11

12

13

np.random.seed(seed=398)

# Draw 10,000 samples out of Poisson distribution: n_nohitters

n_nohitters = np.random.poisson(251/115, size=10_000)

# Compute number of samples that are seven or greater: n_large

n_large = len(n_nohitters[n_nohitters >= 7])

# Compute probability of getting seven or more: p_large

p_large = n_large/len(n_nohitters)

# Print the result

print(f'Probability of seven or more no-hitters: {p_large}')

1

Probability of seven or more no-hitters: 0.0071

The result is about 0.007. This means that it is not that improbable to see a 7-or-more no-hitter season in a century. There have been two in a century and a half, so it is not unreasonable.

Thinking probabilistically: Continuous variables

Probability distributions of discrete variables have been covered so far. This final section will cover continuous variables, such as those that can take on any fractional value. Many of the principles are the same, but there are some subtleties. At the end of this chapter, you will be speaking the probabilistic language required to launch into the inference techniques covered in Statistical Thinking in Python (Part 2).

Probability density functions

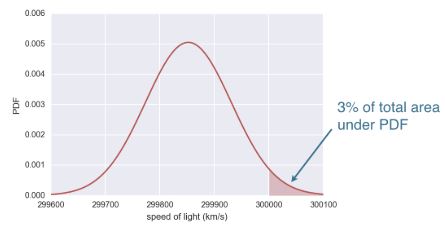

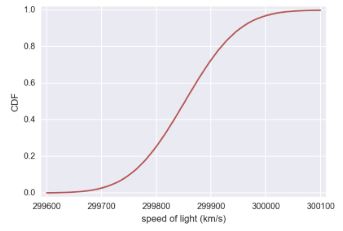

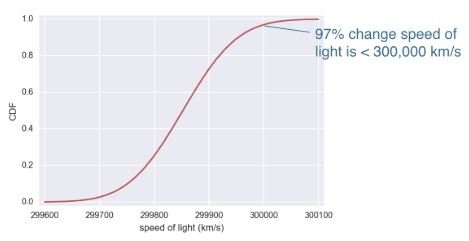

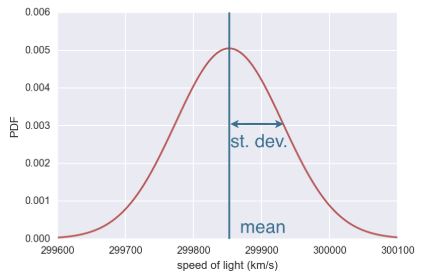

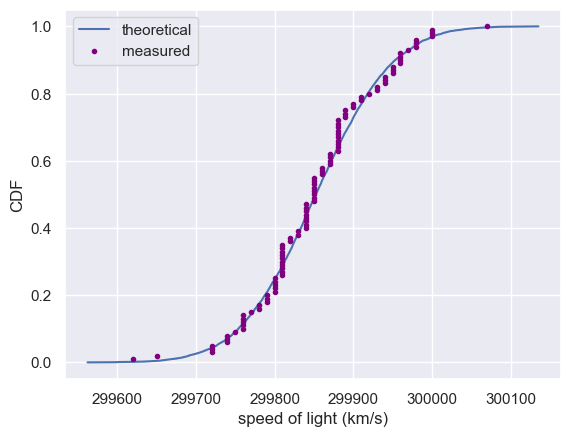

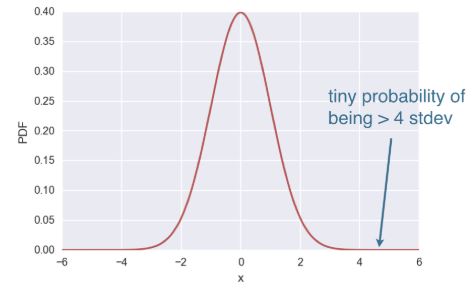

We have talked about probabilities of discrete quantities, such as die rolls and number of bus arrivals, but what about continuous quantities? A continuous quantity can take on any value, not just discrete ones. For example, the speed of a train can be 45.76 km/h. Continuous variables also have probability distributions. Let’s consider an example. In 1879, Albert Michelson performed 100 measurements of the speed of light in air. Each measurement has some error in it; conditions, such as temperature, humidity, alignment of his optics, etc., change from measurement to measurement. As a result, any fractional value of the measured speed of light is possible, so it’s apt to describe the results with a continuous probability distribution. In looking at Michelson’s numbers, show here in units of 1000 km/s, we see this is the case. What probability distribution describes these data? I posit, these data follow the Normal Distribution. To understand what the normal distribution is, lets consider its probability density function (PDF). This is the continuous analog to the probability mass function (PMF). It describes the chances of observing a value of a continuous variable. The probability of observing a single value of the speed of light, does not make sense, because there is an infinity of numbers, between 299,600 and 300,100 km/s. Instead, areas under the PDF, give probabilities. The probability of measuring the speed of light is greater the 300,000 km/s is an area under the normal curve. Parameterizing the PDF based on Michelson’s experiments, this is about a 3% chance, since the pink region is about 3% of the total area under the PDF. To do this calculation, we were really just looking at the cumulative distribution function (CDF), of the Normal distribution. Here’s the CDF of the Normal distribution. Remember, the CDF gives the probability, the measured speed of light will be less than the value on the x-axis. Reading off the value at 300,000 km/s, there is a 97% chance, the speed of light measurement, is less than that. There’s about a 3% chance it’s greater.

We will study the Normal distribution in more depth in the coming exercises, but for now, let’s review some of the concepts we’ve learned about continuous distribution functions.

Continuous Variables

- Quantities that can take any value, not just discrete values

Probability Density Function (PDF)

- Continuous analog to the PMF

- Mathematical description of the relative likelihood of observing a value of a continuous variable

Normal Cumulative Distribution Function (CDF)

1

2

3

4

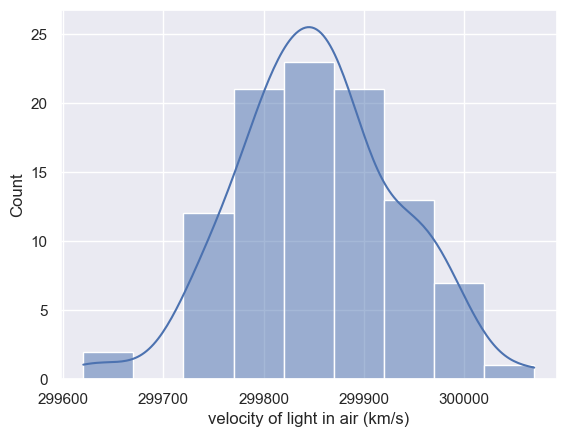

df = pd.read_csv(sol_file)

df.drop(columns=['Unnamed: 0'], inplace=True)

df.columns = df.columns.str.strip()

df.head(2)

| date | distinctness of image | temperature (F) | position of deflected image | position of slit | displacement of image in divisions | difference between greatest and least | B | Cor | revolutions per second | radius (ft) | value of one turn of screw | velocity of light in air (km/s) | remarks | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | June 5 | 3 | 76 | 114.85 | 0.300 | 114.55 | 0.17 | 1.423 | -0.132 | 257.36 | 28.672 | 0.99614 | 299850 | Electric light. |

| 1 | June 7 | 2 | 72 | 114.64 | 0.074 | 114.56 | 0.10 | 1.533 | -0.084 | 257.52 | 28.655 | 0.99614 | 299740 | P.M. Frame inclined at various angles |

1

2

sns.histplot(df['velocity of light in air (km/s)'], bins=9, kde=True)

plt.show()

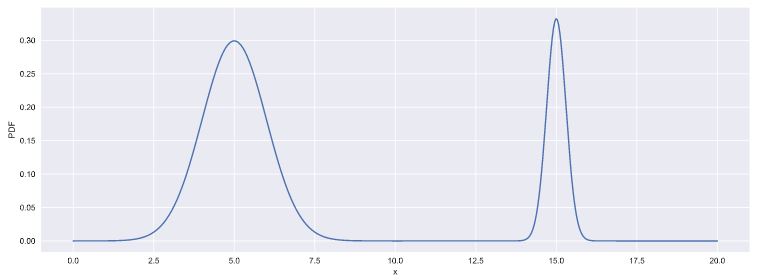

Interpreting PDFs

Consider the PDF shown here. Which of the following is true?

Instructions

- **x is more likely than not less than 10.**

x is more likely than not greater than 10.We cannot tell from the PDF if x is more likely to be greater than or less than 10.This is not a valid PDF because it has two peaks.

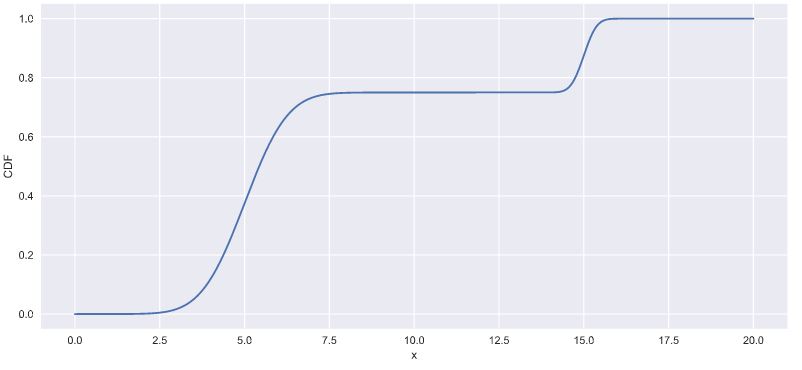

Interpreting CDFs

At right is the CDF corresponding to the PDF you considered in the last exercise. Using the CDF, what is the probability that x is greater than 10?

Instructions

- **0.25: Correct! The value of the CDF at x = 10 is 0.75, so the probability that x < 10 is 0.75. Thus, the probability that x > 10 is 0.25.**

0.753.7515

Introduction to the Normal distribution